Mastering Your Money: The 50/30/20 Budget Rule for Indian Households

Are you an Indian household struggling to make your salary last until the end of the month? Do you often wonder where all your money goes? You're not alone. Many individuals and families face challenges in managing their finances effectively, leading to stress and unfulfilled financial goals. The good news is that achieving financial stability doesn't require complex calculations or a finance degree. It starts with a simple, effective framework: the 50/30/20 budget rule.

This guide will demystify the 50/30/20 rule, explain how it works, and show you how to apply it practically to your Indian household's finances. By the end, you'll have a clear, actionable plan to allocate your income, meet your financial obligations, and build a secure future.

What is the 50/30/20 Budget Rule?

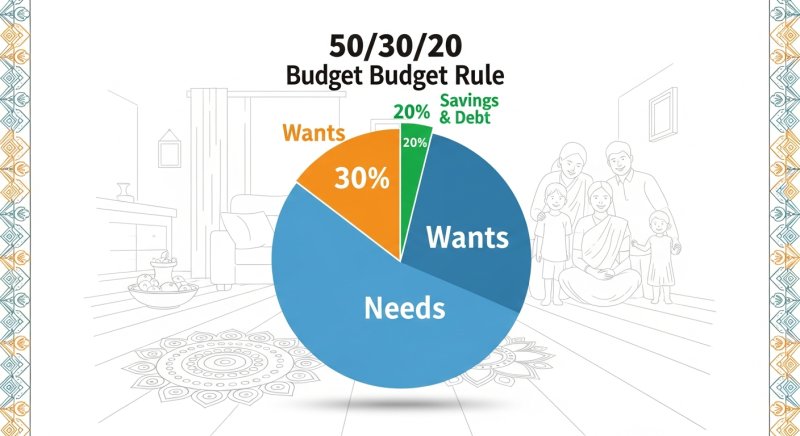

The 50/30/20 budget rule is a straightforward money management guideline that suggests dividing your after-tax income into three main categories:

- 50% for Needs: Essential expenses you can't live without.

- 30% for Wants: Discretionary spending that improves your quality of life but isn't strictly necessary.

- 20% for Savings & Debt Repayment: Funds allocated for financial growth and reducing liabilities.

This rule, popularized by Senator Elizabeth Warren in her book 'All Your Worth: The Ultimate Lifetime Money Plan,' offers a flexible yet structured approach to budgeting, making it accessible for beginners and seasoned financial planners alike.

Breaking Down the Percentages for Indian Households

50% for Needs

Needs are the non-negotiable expenses required to maintain your living standard. For an Indian household, this typically includes:

- Housing: Rent or home loan EMIs.

- Utilities: Electricity, water, gas, and essential internet/mobile bills.

- Groceries: Food and household essentials.

- Transportation: Fuel, public transport, or vehicle EMIs (if essential for work).

- Healthcare: Insurance premiums, essential medicines.

- Minimum Loan Payments: The minimum required payments on any loans (personal loans, education loans, etc.), excluding extra principal payments which fall under savings.

- Children's Education: School fees, essential supplies.

It's crucial to distinguish between a 'need' and a 'want.' For example, while basic internet is a need, a premium streaming service is a want.

30% for Wants

Wants are expenses that enhance your lifestyle but aren't strictly necessary for survival. These are areas where you have the most flexibility to cut back if needed. Examples for Indian families include:

- Dining Out: Restaurant meals, takeaways.

- Entertainment: Movies, concerts, streaming subscriptions.

- Hobbies & Recreation: Gym memberships, club fees, travel.

- Shopping: New clothes, gadgets, non-essential home decor.

- Vacations & Travel: Leisure trips and getaways.

- Premium Services: High-end mobile plans, expensive cable packages.

- Gifts: Non-essential gifts for friends and family.

Understanding your wants is key to finding areas to save money. For instance, if your salary often disappears before month-end, examining your wants can reveal significant opportunities for adjustment. You can learn more about managing this by reading Why Your Salary Disappears Before Month-End: Uncover the Reasons and Take Control.

20% for Savings & Debt Repayment

This category is vital for building long-term financial security and reducing your debt burden. It includes:

- Emergency Fund: Building a safety net for unexpected expenses (aim for 3-6 months of living expenses).

- Investments: SIPs in mutual funds, fixed deposits, stocks, provident fund contributions above mandatory limits.

- Retirement Savings: PPF, NPS contributions.

- Extra Debt Payments: Paying more than the minimum on high-interest loans (e.g., credit card debt, personal loans) to accelerate repayment.

- Goal-Specific Savings: Saving for a down payment on a house, a child's higher education, or a new vehicle.

Prioritizing this 20% ensures you're actively working towards your financial goals and securing your future. For many, this is the most challenging but rewarding part of the budget.

Why the 50/30/20 Rule Works for Indian Households

The 50/30/20 rule is particularly effective for Indian households due to its adaptability:

- Simplicity: Easy to understand and implement without complex financial knowledge.

- Flexibility: While the percentages are a guideline, they can be adjusted slightly based on individual circumstances, income levels, and life stages (e.g., higher debt repayment in early career, more savings later).

- Holistic Approach: It covers all aspects of financial life – essential living, lifestyle choices, and future planning.

- Promotes Financial Discipline: Encourages conscious spending and saving habits.

How to Implement the 50/30/20 Rule (Step-by-Step)

-

Calculate Your Net Income

Start by determining your monthly take-home pay after taxes, provident fund (PF), and any other mandatory deductions. This is the amount you'll be budgeting with.

-

Categorize Your Expenses

Go through all your monthly expenditures and assign them to either 'Needs,' 'Wants,' or 'Savings & Debt Repayment.' Be honest with yourself about what truly constitutes a need versus a want. This step is crucial for understanding where your money currently goes. A helpful resource for this is Your Essential Monthly Expense Tracking Checklist for Beginners.

-

Adjust and Track

Compare your current spending to the 50/30/20 percentages. If you're spending more than 50% on needs, look for ways to reduce them (e.g., finding cheaper rent, cutting down on utility usage). If your wants exceed 30%, identify areas to trim back. Ensure you're consistently allocating at least 20% to savings and debt repayment.

Realistic Example: An Indian Household Budget

Let's consider a couple, Rohan and Priya, with a combined monthly net income of ₹80,000.

- Total Net Income: ₹80,000

50% for Needs (₹40,000)

- Rent/EMI: ₹20,000

- Groceries & Household: ₹10,000

- Utilities (Electricity, Water, Gas, Internet): ₹4,000

- Transportation (Fuel/Public Transport): ₹3,000

- Children's School Fees (basic): ₹3,000

30% for Wants (₹24,000)

- Dining Out/Takeaways: ₹6,000

- Entertainment (OTT subscriptions, movies): ₹3,000

- Shopping (Clothes, gadgets): ₹5,000

- Weekend Outings/Activities: ₹4,000

- Personal Care: ₹2,000

- Miscellaneous Wants: ₹4,000

20% for Savings & Debt Repayment (₹16,000)

- SIPs in Mutual Funds: ₹8,000

- Emergency Fund Contribution: ₹4,000

- Extra Payment on Personal Loan: ₹4,000

By following this allocation, Rohan and Priya can manage their current expenses while actively building their financial future.

Tips for Success with the 50/30/20 Rule

- Automate Your Savings: Set up automatic transfers from your salary account to your savings/investment accounts the moment you get paid. This ensures you pay yourself first.

- Review Regularly: Life circumstances change. Review your budget monthly or quarterly to ensure it still aligns with your income and goals.

- Be Flexible, Not Rigid: The percentages are guidelines. If you have a major financial goal (like buying a house), you might temporarily shift more towards savings (e.g., 40/30/30).

- Cut Down on Wants First: If you find yourself overspending, always look to reduce your 'wants' before compromising on 'needs' or 'savings.'

- Track Every Rupee: Knowing exactly where your money goes is the cornerstone of effective budgeting.

To effectively implement the 50/30/20 rule and gain clear visibility into your financial habits, a reliable tool is invaluable. Depto Flow helps you accurately track your income and expenses, allowing you to categorize them easily into Needs, Wants, and Savings. This way, you can see if you're sticking to the 50/30/20 percentages in real-time and manage your budget effortlessly. Download Depto Flow today to start your journey towards financial mastery: https://flow.depto.in/app/download-app.

Conclusion

The 50/30/20 budget rule is a powerful yet simple framework that can transform your financial life. By clearly allocating your income into needs, wants, and savings/debt repayment, you gain control, reduce stress, and accelerate your progress towards financial freedom. It provides a clear roadmap, especially for Indian households navigating diverse financial landscapes.

Start by understanding your current financial situation, apply the 50/30/20 framework, and use tools like Depto Flow to track your progress. Take the first step today to gain clarity and control over your money. Download Depto Flow and begin your journey to a more secure financial future.